We are long SPWR, ENPH, DQ, ENVX shares. This article does not constitute investment or trade advice. We share our analysis as documentation for our own investing decisions, which might turn out to be underperforming the market. Micro-caps are volatile investments. Complete loss of capital is a possibility.

Trade

Long SunPower ($SPWR)

Date: 10/10/2025

Symbol: SPWR

Order: BUY

Entry Price: $1.61

Position size: Full

Time horizon: 5 years+

Price Target

5-year target (2030): $13.00 (+907%)

Summary

The US is dangerously behind China in terms of electricity generation.

“Winning the A.I. race” has been deemed existential by the current administration, and energy is one of the key inputs for A.I.

Solar, while only a partial solution, has many interesting properties and strong tailwinds.

A few of the surviving solar U.S. companies could generate outstanding returns as they consolidate and help fill the immense gap in electron generation.

Supporting Trends

The US-China Rivalry

The US is dangerously behind China in terms of power output. In 2024, China generated over 10,000 TWh of electricity. That is more than the combined output of the U.S., the EU, and India (the next three largest producers). China's economy used 81% more energy than the US economy in 2023. More troubling is how much electricity generation capacity China is adding every year, while the U.S. energy production has been mostly stagnant. The difference in electricity generation between China and the US

Discussions

China has risen to be a serious contender, if not the leader, in many of the bleeding-edge technologies, such as EV cars (e.g, BYD), A.I. (e.g, DeepSeek), robotics, drones, and solar panels. We won’t dive deeper into the implications of US-China rivalry in this article, but most should understand it has deep implications for an active investor over next decades.

The Inevitable Demand for More Energy

The AI race is deemed existential for the survival of the American Empire. This has been publicly stated in podcasts by President Trump’s close advisor, David Sacks, also known as the White House AI & Crypto “Czar”.

This article is not an endorsement of any political party, by the way. We view the US-China rivalry and the evolving global order as long-standing trends that transcend the US two-party system.

If the US wants to “win” the so-called “AI race” and build data centers and automated factories, the US needs to overhaul its energy infrastructure dramatically.

Some will argue that newer AI models and newer GPU chips will be way more efficient and consume a lot less energy than today.

It’s a valid argument, but if we were to believe in the Jevons Paradox, lower cost of inference and training will also lead to mass commoditization and overall higher energy use. AI’s demand curve is extremely elastic: cheaper compute invites new use cases (AI-generated videos, workface agents, personalized models), which multiply total energy demand.

Robots and the electrification of all transportation will also continue to demand more energy input.

Most would recognize that this is bullish for many forms of energy production in the US, including: fossil oil & gas, nuclear, and renewable energy. On that note, we’ve written how we invested earlier in Aemetis (Renewable Biofuels).

What about fusion? Fusion on Earth is likely decades away from being commercially available, while we already have a working fusion reactor over our head we can use today, the Sun.

Why Solar, and Why Now?

A 4-year bear market

Since 2021, the solar industry in the US has been in a price bear market. For example, the TAN solar ETF has lost almost -77% from its recent peak in January 2021 to the low in April 2024.

TAN ETF price

Enphase ($ENPH) is an industry leader in solar micro-inverters, which convert the direct current (DC) electricity generated by solar panels into alternating current (AC) electricity for homes and businesses. The stock has lost 89% since its 2022 peak. Enphase stock price

What are the factors that could have caused this bearish price action in the last 4 years?

The Covid Bubble: It could be argued that the 2020-2021 period was a period of excessive optimism. Solar and “green/clean tech” stocks had been bid up aggressively on excitement over a clean-energy transition.

Higher for longer: A key factor weighing on the industry has been the rising interest rate environment since 2021.

Supply chain vulnerabilities, exacerbated by the global pandemic and geopolitical tensions, have also played a significant role. The industry has grappled with volatility in the price and availability of key materials, including polysilicon, a critical component in solar panels.

Uncertain Subsidies: U.S. federal incentives (e.g., Investment Tax Credit, bonus credits under the Inflation Reduction Act) face political threats, phase-outs, or more restrictive rules. As detailed later in this article, we take the contrarian view that subsidies going away is not necessarily a bad thing.

It’s important to distinguish, however, between solar stock indices/equities and solar deployment/project growth.

The Demand is Still Here and Growing

Over the last decade, the U.S. solar industry has seen an average annual growth rate of 28%.

In the first half of 2025 alone, the U.S. solar industry installed nearly 18 GW of new capacity, with solar and energy storage accounting for a dominant 82% of all new power added to the grid. Projections indicate that the American solar industry will add an average of 43 GW of new capacity annually through 2030.EIA:Solar generation was 3% of U.S. electricity in 2020, but we project it will be 20% by 2050

Solar's Unique Properties

Intermittent energy, but more and more viable

Data centers need stable energy, but solar is an intermittent source. Nonetheless, augmenting solar output for residential usage will reduce the load on the grid, which can redirect more electrons to data centers.

With the current and future advances in battery tech, solar is an increasingly viable source for many homes and companies.

The decentralization and resilience of the grid

Picture the image of a home with solar panels on its roof. It charges batteries at night. It charges one or two EV cars

Instead of having millions of houses only depending on a grid, which can be disrupted by climatic events, or worse, solar energy enables the decentralization of the power grid.

On the opposite, nuclear plants are centralized and vulnerable nodes, as we have seen in the war in Ukraine. That doesn’t mean we are not bullish on nuclear energy as well; we are just pointing out the interesting differentiating factors of solar.

Green electrons for the environmentalists

An EV owner can decide to charge the car with only renewable energy, bypassing the grid and other sources of energy completely. Being low-carbon or zero-carbon emission is a demand from a part of the population, which we argue will be growing.

Enphase software allows neat visualization and control of the energy production.

Cheap energy that can ramp quickly

Another advantage of solar is that it is one of the cheapest energy sources available right now, and it doesn’t require years of construction.

Below's a comparative table of typical Levelized Cost of Electricity (LCOE) estimates for various generation sources.

Generation Type

Representative LCOE Range (USD/MWh)

Solar PV (utility-scale, without storage)

~ 29 to 92

Solar PV + 4-hour battery storage

~ 60 to 210

Onshore wind

~ 24 to 75

Gas, combined cycle (new)

~ 45 to 108

Coal (new / with emissions controls)

~ 69 to 168

Gas peaking (open cycle turbines)

~ 110 to 228

Nuclear (new builds / “nth of a kind”)

~ 141 to 220

Lazard reports an average of ~$61/MWh for utility solar in 2024 (unsubsidized) inRenew Economy

Batteries obviously increase cost, but we have to anticipate a significant price drop in future battery technologies.

The New SunPower is Positioned for Great Returns

We have assumed that there will be a dramatic energy output increase in the US, and that solar could be one of the many beneficiaries. We want to find one or a few stocks in the industry that we think will not only survive, but thrive and achieve great risk-adjusted returns.

We became interested in a micro-cap formerly called “Complete Solaria” last year.

Complete Solaria was founded by Will Anderson in 2010. In 2024, T.J. Rodgers, a veteran Silicon Valley entrepreneur and former head of Cypress Semiconductor, became CEO and chairman, investing directly and leading the revival of the company. The company gained prominence by acquiring key assets from the bankrupt SunPower in 2024, and in 2025 rebranded itself under the SunPower name.

T.J. Rodgers is a veteran entrepreneur who has been involved in a myriad of companies, such as the Old SunPower, Enovix, a novel battery architecture, and Enphase, the leader in solar inverters.

At its core, the new SunPower is a U.S. residential solar technology, services, and installation firm.

SunPower makes its revenue and profit from installing solar panels for residential homes and companies. While solar panels might not be completely manufactured in the US, their installation and servicing cannot be offshored, and this is where the margins come from.

If we assume the solar market will continue to grow strongly in the U.S., SunPower has a lot of room to grow.

What makes it interesting to our eyes is the current valuation (a $154M company) and its potential to become a $1.5B+ company. Old SunPower was at some point a $9B company, before mismanagement ran it to the ground. We are talking about an 8-10x potential in 3 years, with possibly much more upside in the longer term, so let’s dive in to see what the likelihood of that is. Can T.J. Rodgers rebuild an ultra-competitive machine?

The Investment Case on SunPower

Bold ambitions

The company’s mission (extracted from Earnings Call slide) reads:

“Consistently profitable growth from $300m in 2025 to 1B$ in 2028 using organic and inorganic growth while remaining consistently profitable”.

And the company’s vision:

“SunPower is again recognized No. 1 in solar. SunPower has regained its traditional technology superiority buy creating software-controlled intelligent solar system products that dominate an industry that has degraded to commodity sales and government handouts.”

It’s important to point out T.J.'s disdain for government subsidies, which, according to him, created bloated and inefficient companies in the industry. This also increased the cost for the end-consumer, who couldn’t benefit from efficient market pricing.

The thesis of betting on solar is not because of government future handouts; it is because the technology is so useful and needed.

A Bet on T.J. Rodgers

A bet on SunPower is obviously first and foremost a bet on its new CEO and its unique personality and vision, and for him to be able to bring SunPower back to its former glory. aa

T.J., 77, as of today, has been an incredibly successful Silicon Valley entrepreneur and Venture Capitalist. He has a PhD in electronics, founded Cypress Semiconductor, and took it public in 1986. He has been involved in Old SunPower, in the Enphase turnaround, and Enovix as chairman. He has decided to come out of retirement and lead the new SunPower. This might be his last rodeo.

Running the company like a Silicon Valley startup

T.J. emphasized running the company like a startup, and that means incentivizing employees with stock grants, binding the success of the company with their hard work.

From the vision statement, SunPower wants to reach technological superiority again (software and hardware), with innovation being crucial for competitiveness.

Lean operations

The CEO implemented dramatic cost reduction after the Complete Solaria and SunPower merger, and tight control on headcount, which is scrutinized every week. This aligns with the mission statement to be profitable every quarter with no exception.

Slide from the company presentation showing headcount targets

The Elon Musk playbook comes to mind, where he cut 2/3 of the old Twitter headcount.

The cost-cutting extends to some divisions, for example, some of the financial accounting was offshored in India.

Very high standard of quality

The stated goal is to have 100% first pass yields, and for that to keep the Quality Department at its current headcount (18).

Profitability every quarter

From the last earnings calls, we can see that the leaning of operations have helped the company achieve profitability every quarter since Q4 2024.

Source: company's IR slides

The Path for Growth

The management has shared during earnings calls the two main paths for revenue growth, organic and inorganic.

The organic path has been to rebuild a pipeline of new home bookings. There have been discussions on improving Sales Efficiency, with the nomination of Dan McCranie – a sales veteran, as the EVP of Marketing & Sales.

Source: company's IR slides

The Battery Angle: SunPower can also sell batteries as part of its offering, which will significantly increase its gross margin. The attach rate of battery is 99% in CA, and 50% in the US. SunPower's current attach rate is only at 14%, so there is a lot of upside potential.

The inorganic growth plan relies on strategic acquisitions. Merging under SunPower's umbrella few private solar companies can open new markets and bring unique technologies, expertise, and talent.

SunPower, for example, recently acquired Sunder, making it the 5th Solar company in the US. This dramatically changes the coverage of US states.

Source: company's IR slides

SunPower has been a strong brand that has commanded higher prices. It can make sense for some smaller private solar companies to join a public company if synergies can be created.

Source: company’s IR slides

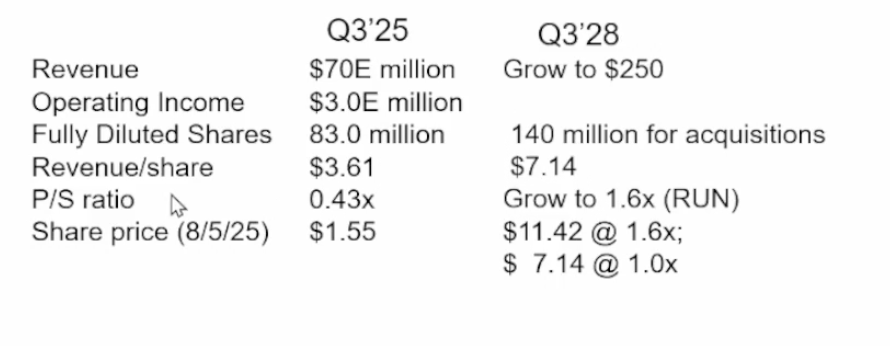

Valuation and Potential

SunPower is currently at a P/S ratio of 0.44x, while other top solar companies like Enphase and SolarEdge command an average P/S ratio of 2.0x+.

A comparison of P/S and competitors. Source: company’s IR slides

Normalization of the P/S ratio above 1.6x when the concerns about the company's survival subsides is also what would make the stock price significantly appreciate.

A breakdown of the revenue target for Q3 28. Source: company’s IR slides

At the 2028 projected revenues of $1B, accounting for the dilution of shares for acquisitions (+70% outstanding shares), the share price would be at $11.42 at a 1.6x valuation.

For reference, Old SunPower had $1.7 billion of revenues in 2022 at a 3B$ valuation, before going bankrupt in 2024 with a mountain of debt.

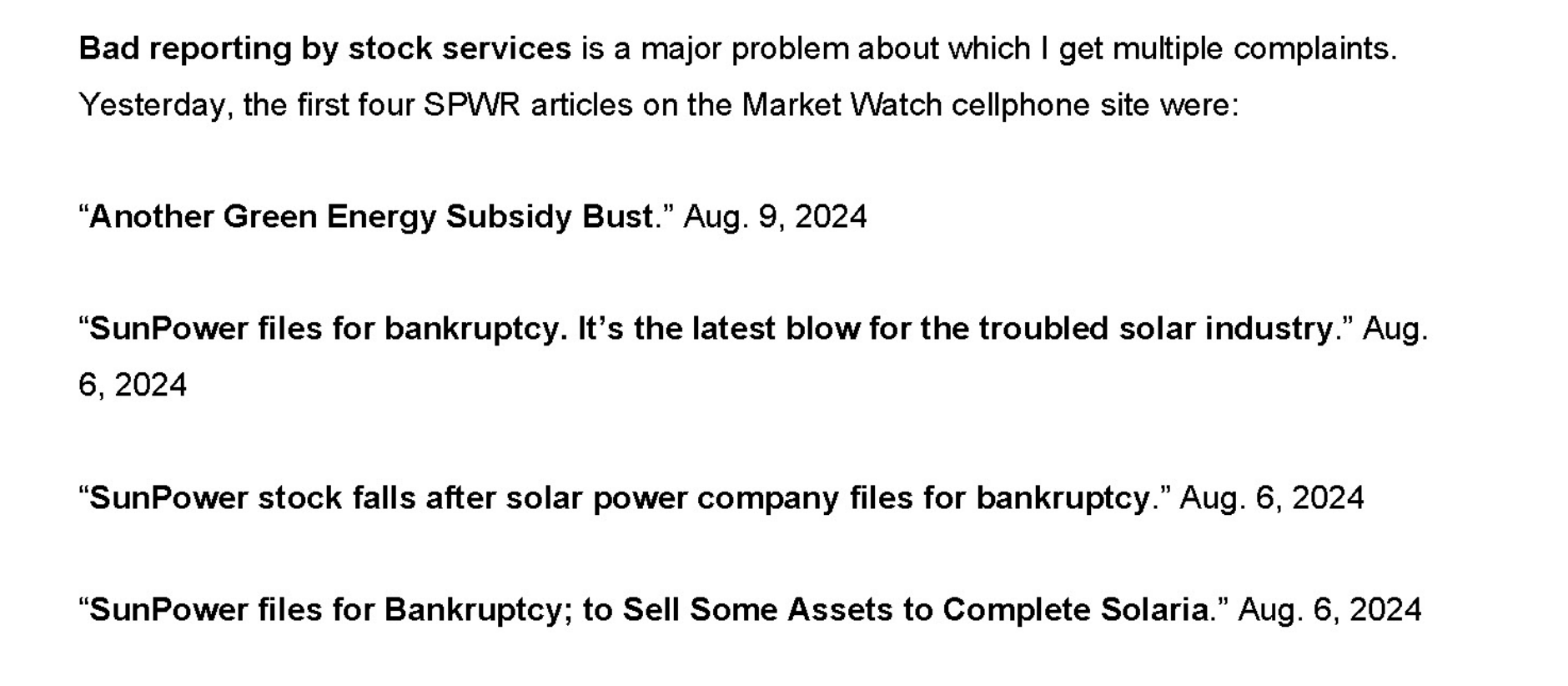

Under the Radar stock

With the Old SunPower bankruptcy, the stock is just not very well covered yet by analysts. It’s also a micro-cap, which means many institutional investor won’t invest in it, for compliance reasons.

From the Earning Calls slides, what comes up in the search on the name “SunPower”.Source: company’s IR slides

We view the bad press as a formidable opportunity to load up shares at cheap prices.

Risks

Competitive and Market Pressures: The residential solar industry is intensely competitive, characterized by thin margins and a constant need for innovation. SunPower faces established competitors in a market susceptible to economic downturns and fluctuating consumer demand. SunPower's ability to differentiate itself through technology and service will be crucial for its long-term success.

Integration and Execution Risks: The current iteration of SunPower is a composite of Complete Solar, acquired assets from the "old" SunPower (including the brand, Blue Raven Solar, and the New Homes division), and the recently acquired Sunder Energy. Integrating these disparate entities, each with its own culture, operational processes, and customer base, presents a significant challenge. Failure to effectively integrate these components could lead to operational inefficiencies, customer dissatisfaction, and a failure to realize the anticipated synergies of the acquisitions.

Forward-Looking Statements and Projections: Recent announcements from the "new" SunPower's leadership have expressed optimism about future revenue and profitability, particularly following the Sunder Energy acquisition. However, these are forward-looking statements and are not guarantees of future performance. Investors should critically evaluate these projections in light of the inherent risks and uncertainties of the solar market and the company's recent history.

Tariff's impact: While module assembly has increased in the US, the more complex, upstream manufacturing stages (polysilicon, wafer, and cell production) still lag well behind demand. The U.S. continues to rely heavily on imported solar cells to feed its domestic module assembly plants.

Other investment ideas

Enphase ($ENPH): the US leader of solar micro-inverters. Enphase's foundational competitive advantage lies in its micro-inverter technology, which fundamentally differs from the traditional string inverter systems used in many solar installations (e.g., SolarEdge). Competitors include Tesla.

Tesla ($TSLA): another leader in solar, batteries, and micro-inverters, but also diversified into many other segments (EV, robotics, AI).

Daqo New Energy Corp ($DQ): a leading Chinese manufacturer of high-purity polysilicon and monocrystalline silicon (mono-Si), which are the fundamental raw materials used to make solar cells and modules (solar panels).

Conclusion

We are looking to ride the general trend of higher energy generation in the US and invest in a few stocks that could benefit greatly.

The potential strong growth of the US solar market, coupled with the current lack of investor interest in the sector, makes it a potentially compelling contrarian bet.

We’ve invested in some other “T.J. Rodgers-related companies” (Enovix, Enphase), and we like the solar focus of his new company. We also appreciate T.J. Rodgers' brash personality and unique communication style with the stakeholders.

We initiated a position in SPWR a few months ago at 1.43, and we are increasing our position while the price is below 1.90.

Investments in micro-cap stocks can be quite volatile, and we fully expect wild price swings, especially if the general market is selling off, which we are expecting could happen in Q4 2025 or 2026. That could send the stock price well below 1.30, which we will probably view as another buying opportunity, unless something fundamental has changed.

Our 5-year minimum target, based on revenue growth and PE ratio expansion: 13.00

-

Thank you for reading, we hope you've learned a thing or two, even if you disagree with the investment case.

What do you think are the best ways to play the US-China rivalry and Energy Gap ? Let us know in the comments.

Residential solar is a crowded market, with many competitors. Margins are thin. The article argues premium brand / software + hardware could differentiate, but that is easier said than done.

The difference in electricity generation between China and the US

The difference in electricity generation between China and the US